As long as the Iran conflict continues, the Strait of Hormuz remains closed, and energy facilities in the Middle East face damage, the world is likely to see shortage of both oil and gas. The resulting increase in prices is likely to have a significant impact on the global economy which prior to 28th February 2026 was showing signs of growth. The world is facing considerable uncertainty going forward, which does not bode well.

A WORLD WITHOUT OIL AND GAS!

The Iran war

The war between the US and Israel on one side, and Iran on the other, has been ongoing since 28th February 2026, and after almost 2 months, a ceasefire is in place, although there continue to be skirmishes. Pakistan took on the mantle of attempting to broker a peace deal and arranged a meeting between the US and Iran on 10th April. The talks ended after approximately 21 hours with no resolution in sight. A second round of talks in the third week of April did not take off.

The conflict has seen both sides bombarding each other (in the case of the US, the brunt of Iran’s fire struck the Gulf countries which housed American bases). There has also been damage to oil and gas facilities in the region which could have long lasting implications on the world’s supply of the products.

Iran’s stance on the Strait of Hormuz effectively put a dent in 20% of the world’s oil supply with many countries introducing emergency measures to cope with potential shortages. While, passage through the Strait was re-introduced for 2 weeks during the ceasefire, there is no guarantee that this will remain into the future and Iran is levying a toll of USD 2 million (apparently payable in Chinese Yuan) per ship using the route. The fact that the US has also started a blockade of the Strait has meant that almost no ships are being allowed to cross.

Perhaps of more concern is the damage that has been caused to various oil facilities in the Middle East, both in Iran and the GCC. EnergyNow.com reports extensive damage to oil refineries during the first 40 days of the conflict, although some have been restarted. The countries that have been impacted are Saudi Arabia, Bahrain, Kuwait, and Iraq. Gas facilities that have been affected are in Qatar (who used their force majeure clause), the UAE, and Iran. Oil fields in Iraq and Saudi Arabia were also hit by missiles or drones but it seems with minimum damage. Ports in the region have also been impacted although by all accounts only suffered temporary disruption.

It has been estimated that as much as 10% of the world’s oil supply was lost and repairs to the sites could cost in excess of USD 25 billion – a staggering amount! In addition, and even more concerning, Qatar’s LNG facility has suffered significant damage. A number of facilities that were hit are witnessing an environmental issue “smog and pollution have blocked out the Sun and left a strong smell of burning in parts of the city, while experts warn the scale of some of the pollutants released could be unprecedented”, reports the BBC in respect of Iran. Residents in the area have also reported “black rain”.

Where are the major oil and gas reserves?

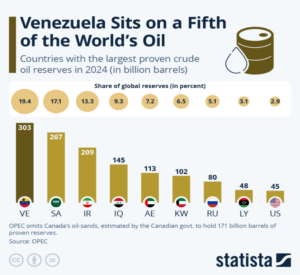

Venezuela is estimated to have 20% of the world’s crude oil with 303 billion barrels, although in 2025 the country only provided 1.3% of the world’s supply. Saudi Arabia, Iran, and Iraq, in that order, supply 621 billion barrels, bearing in mind that this was before the current conflict and the comments above. These numbers are quoted by Statista from the OPEC 2024 report. The report does not include Canada’s oil sands which provides 171 billion barrels. According to OPEC, in 2024 the US led global production at 18.2%, followed by Russia at 12.7% and Saudi Arabia at 12.3%.

Worldometer estimates oil reserves in 2025 at 1.7 trillion barrels but according to their website, current reserves sit at 1.3 trillion barrels. At consumption levels in 2024, there are 47 years of oil remaining.

However, and this is the key statistic given the current conflict, as much as 47% of the world’s oil reserves in 2025 came from the Middle East – Saudi Arabia, Iran, Iraq, the UAE, and Kuwait. If the conflict continues, the world may witness a significant reduction in supply.

Source: Statista https://www.statista.com/chart/16830/countries-with-the-largest-proven-crude-oil-reserves/

Turning to natural gas and the position appears to be even more dire. The product is considered one the most critical sources of energy being cleaner than coal and oil. The three largest sources of natural gas are thought to be Russia, Qatar, and Iran, and all three are in the midst of a conflict! In fact, 15 countries are estimated to hold 87% of the planets proven reserves. Of these 4 are in the centre of the current conflict which probably has over 50% of the reserves.

Clearly, both oil and gas supplies are under severe threat with the Iran conflict which could have a significant impact on global supply if sites are damaged. A daunting prospect to say the least.

Closer to home, there are reserves of oil and gas but a considerable amount is yet to be done to reach the production stage.

The first oil shock and the introduction of the “Petro Dollar”

In October 1973, a phenomenon colloquially known as the “Arab oil embargo” began which saw oil shipments from the Middle East to a number of countries stop because of their support for Israel in the Yom Kippur War. This event was thought to be the first oil shock the world had seen resulting in a significant increase in global prices and an energy crisis of unimaginable proportions, at least until 2026. At around the same time, the then US President, Richard Nixon, shunned the gold standard which saw a devaluation of the US Dollar. This had a significant impact on the profits of the oil producing nations.

The embargo against the US was stopped in March 1974 by which time global oil prices had quadrupled, and indeed rose ten-fold during the Seventies, leading to shortages of fuel and a steep increase in pump prices. The events of the six months between October 1973 and March 1974 saw the birth of the “Petro Dollar” coupled with Saudi Arabia agreeing to use the US Dollar for its oil sales in exchange for US military protection. The Petro Dollar has been in place since then but changing geo-politics, but the move to what could be known as the“Petro Yuan”, and Climate Change moving towards clean renewable energy, has put the 50-year standard under pressure.

|

“So oil and gas [are traded in dollars], but then also downstream with all the derivatives, but then also all the chemical elements derived from the oil industry and petrochemical industry. And then likewise, upstream with all the technology and inputs required to extract the oil, [it] created a dollar-denominated value chain with global and international repercussions”. Andrés Arauz, former Ecuadorian Minister and Central Bank Director to Green Central Banking |

The advantage for the US has been that surplus US Dollars in the oil and gas producing currencies are generally recycled back to the US by investment in Treasury instruments and equities. In essence, the Petro Dollar has meant that the US Dollar has been the anchor of global trade for the past 50-plus years.

However, there does appear to be significant pressure on the Petro Dollar system and the world is beginning to see a shift, that may well be accelerated with the current conflict in the Middle East. Green Central Banking report that the “dollar’s share of global reserves has declined from 71% to 56.3% since 2008, with Central Banks purchasing over 1,000 metric tons of gold annually for three consecutive years”.

The BRICS countries, which expanded in the last two years to include Egypt, Ethiopia, Iran, UAE, and Indonesia, are in the midst of coming up with a new financial mechanism to allow for trading within the bloc. The group has already established the New Development Bank for infrastructure projects which will extend to other countries. Suffice to say that all could be done without the US Dollar.

A number of countries have in the past year or so liquidated their US Treasury holdings with China reported to have reduced from USD 1.3 trillion in 2013 to USD 682 billion in November 2025 and at the same time increasing Yuan based trade in Asia, with a gradual shift to other parts of the world. Even the European Central Bank President, Christine Lagarde, said in May 2025 that, may be the time for a “global Euro moment” is on the cards.

With most sovereign loans denominated in the US Dollar, the increase in oil prices currently being seen, will mean increased debt burden. This will have a critical impact on the African Continent which is heavily indebted.

The second oil shock and the move to the “Petro Yuan”

While there have been ups and downs in the oil and gas sector throughout history, the second major shock is perhaps the current crisis in the Middle East. The closure of the Strait of Hormuz has impacted as much as 20% of the world’s oil supply and perhaps as much as 50% of the gas output. Clearly, an interruption of this magnitude has had an impact on prices and supply.

Iran had been allowing ships to cross the Strait but only those belonging to what the country says are its “allies” which translates roughly to those who do not support the current conflict in Iran. China is one such country and the transactions are happening using the Chinese Yuan. Indeed, Bloomberg quotes a strategist at Deutsche Bank as saying: “The conflict could be the catalyst for erosion in petrodollar dominance and the beginnings of the PetroYuan”. As mentioned above, recent events have seen a reduction in crossings as both Iran and the US have set up blockades.

|

“Damage to Gulf economies could encourage an unwind in their foreign asset savings. In this context, reports that the passage for ships through the Strait of Hormuz may be granted in exchange for oil payments in Yuan should be closely followed. The conflict could be remembered as a key catalyst for erosion in PetroDollar dominance, and the beginnings of the PetroYuan”. Deutsche Bank quoted in Fortune |

However, and to be fair, there have been times in the past when the demise of the US Dollar was discussed but never materialised. It has continued to be the dominant currency since 1974 but it seems the current situation could well bring about changes. Only time will tell if the world has reached a tipping point. Suffice to say a number of trade deals around the world are happening without the use of the US Dollar, a prime example being India’s purchase of Russian oil. Iran’s move to only sell its oil in Chinese Yuan is likely to have long-term impact on the Petro Dollar. Deutsche Bank has said: “A move away from oil could be as powerful as the pressure to price it in other currencies. A world that becomes more self-sufficient in defence and energy could also be a world that holds less USD reserves.”

What is clear today, is that many countries are facing the brunt of the closure of the Strait of Hormuz and there may well be a shift to other forms of energy for the future. Electric vehicles are rapidly becoming the flavour of the month.

The cost of oil and gas

When the Russia-Ukraine crisis began in 2022, Brent crude oil prices saw a significant increase but stabilised shortly thereafter.

The Iran conflict has seen a similar spike and while it has been going for a shade under 2 months now, there is no telling how much further they will spike. What is clear is that the world is seeing a shortage on the horizon which shows no sign of abatement. The world is bracing itself for an economic downturn and the return of inflationary pressures. A similar picture is seen in the price of natural gas which will have the same impact of the global economy.

The future?

As long as the Iran conflict continues, the Strait of Hormuz remains closed, and energy facilities in the Middle East face damage, the world is likely to see shortage of both oil and gas. The resulting increase in prices is likely to have a significant impact on the global economy which prior to 28th February 2026 was showing signs of growth. The world is facing considerable uncertainty going forward, which does not bode well.

This is a commentary and comments are welcome by email to: info@eaa.co.ke . The views expressed here are not necessarily those of the Association.